ASEAN Economic Issues (December 2023)Trade & Investment Unit, ASEAN-Korea Centre

1. Korea’s Trade to ASEAN Countries

Unit: 1 million (USD)

| Country/Region |

November 2023 |

November 2022 |

2022 |

| Export |

Import |

Total |

Total |

Total |

| Total (Korea) |

55,776 |

51,998 |

107,775 |

110,620 |

1,414,954 |

| ASEAN |

9,824 |

6,126 |

15,950 |

15,227 |

207,418 |

| Brunei Darussalam |

7 |

121 |

127 |

5 |

345 |

| Cambodia |

47 |

38 |

86 |

71 |

1,051 |

| Indonesia |

812 |

897 |

1,708 |

1,921 |

25,951 |

| Lao PDR |

9 |

5 |

16 |

8 |

150 |

| Malaysia |

941 |

1,247 |

2,188 |

2,024 |

26,723 |

| Myanmar |

25 |

31 |

57 |

70 |

1,013 |

| Philippines |

763 |

403 |

1,166 |

1,232 |

17,484 |

| Singapore |

1,704 |

852 |

2,555 |

2,065 |

30,553 |

| Thailand |

590 |

536 |

1,125 |

1,235 |

16,461 |

| Vietnam |

4,926 |

1,994 |

6,921 |

6,596 |

87,688 |

| China |

11,356 |

12,086 |

23,442 |

23,507 |

310,366 |

| Japan |

2,565 |

3,718 |

6,283 |

6,615 |

85,318 |

Reference: Korea Customs Service

(Overall) Korea exported $55.8 billion (7.8%), imported $52.0 billion (-11.6%), and recorded a trade surplus of $3.8 billion. In November 2023, exports surpassed the year’s highest performance within just one month, achieving positive export growth for the second consecutive month.

(By country) ASEAN exports maintained a two-month consecutive growth trend, with exports to the United States, achieving a record-high performance of $10.9 billion, and exports to China also reaching the highest performance of the year at $11.4 billion.

(By category) Exports of Semiconductor, along with 12 other items, saw an increase, reaching the highest export volume of the year.

(Korea’s trade surplus) US ($4.74 billion), ASEAN ($3.7 billion), Vietnam ($2.93 billion), Japan ($1.15 billion).

(Policy Direction) According to the Minister of the Ministry of Trade, Industry, and Energy, despite challenging external conditions, both exports and trade surplus have achieved their highest records this year. Emphasizing this accomplishment, the Minister announced plans to address financial burdens faced by small and medium-sized enterprises such as high interest rates and prolonged economic challenges. The Ministry intends to introduce an ‘Export Preferential Guarantee Package’ by the year-end and focus on organizing export consultations and exhibitions to bolster overseas marketing initiatives. (Link)

2. 2023 Korea’s Overseas Direct Investment to ASEAN Countries (Q3)

| Country/Region |

2022 |

2023 |

| Q1 |

Q2 |

Q3 |

Total |

Q1 |

Q2 |

Q3 |

Total |

| Total (Korea) |

28,221 |

19,845 |

18,374 |

66,440 |

16,893 |

15,649 |

14,623 |

47,165 |

| ASEAN |

2,219 |

2,248 |

1,667 |

6,133 |

1,267 |

2,316 |

1,499 |

5,082 |

| Brunei Darussalam |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

| Cambodia |

19 |

163 |

63 |

245 |

131 |

47 |

54 |

232 |

| Indonesia |

387 |

208 |

420 |

1,016 |

257 |

855 |

420 |

1,533 |

| Lao PDR |

19 |

31 |

9 |

59 |

3 |

9 |

13 |

26 |

| Malaysia |

167 |

52 |

108 |

328 |

64 |

48 |

51 |

164 |

| Myanmar |

112 |

88 |

101 |

301 |

45 |

56 |

38 |

139 |

| Philippines |

31 |

15 |

18 |

64 |

25 |

22 |

32 |

79 |

| Singapore |

1,034 |

799 |

388 |

2,220 |

243 |

399 |

237 |

880 |

| Thailand |

45 |

37 |

20 |

102 |

45 |

17 |

67 |

130 |

| Vietnam |

403 |

855 |

540 |

1,798 |

454 |

863 |

584 |

1,901 |

Reference: Korea Eximbank

(Overall) In the third quarter of 2023, South Korea’s overseas direct investment, based on total investment, recorded $14.6 billion—a 20.4% decrease compared to the same period last year, which amounted to $18.3 billion.

(By region) During the third quarter of 2023, investment levels decreased across all regions compared to the same period last year, with a notable 43.8% reduction observed in the Asian region compared to the previous year.

(By country) Among ASEAN countries, investments in Vietnam and Indonesia have increased (by 8.3% and 0.1% respectively), compared to the same period last year. Meanwhile investment in Singapore, the top investment country, decreased by 28.8%. Among the top investment target countries, the US secured the top position with $6.68 billion, while Vietnam claimed the fifth spot with $580 million.

(By industry) The sectors receiving the most substantial investments were ranked as follows: financial and insurance services, real estate, scientific, and technical services.

(Analysis) During the third quarter, foreign direct investment continued its downward trend, influenced by factors such as the prevailing high-interest rates in major economies and concerns about economic slowdowns in Europe and China. Meanwhile, investments in industries related to the North American and ASEAN regions for securing a foothold in the secondary battery market and strengthening supply chains are showing a sustained trend. Investments toward China, on the other hand, remain in a state of decline.

3. ASEAN Matters for America/America Matters for ASEAN (Link)

Written by East-West Center in Washington (Part of the Asia Matters for America Initiative)

In cooperation with US-ASEAN Business Council and ISEAS-Yusof Ishak Institute

1) Trade Agreements and Frameworks

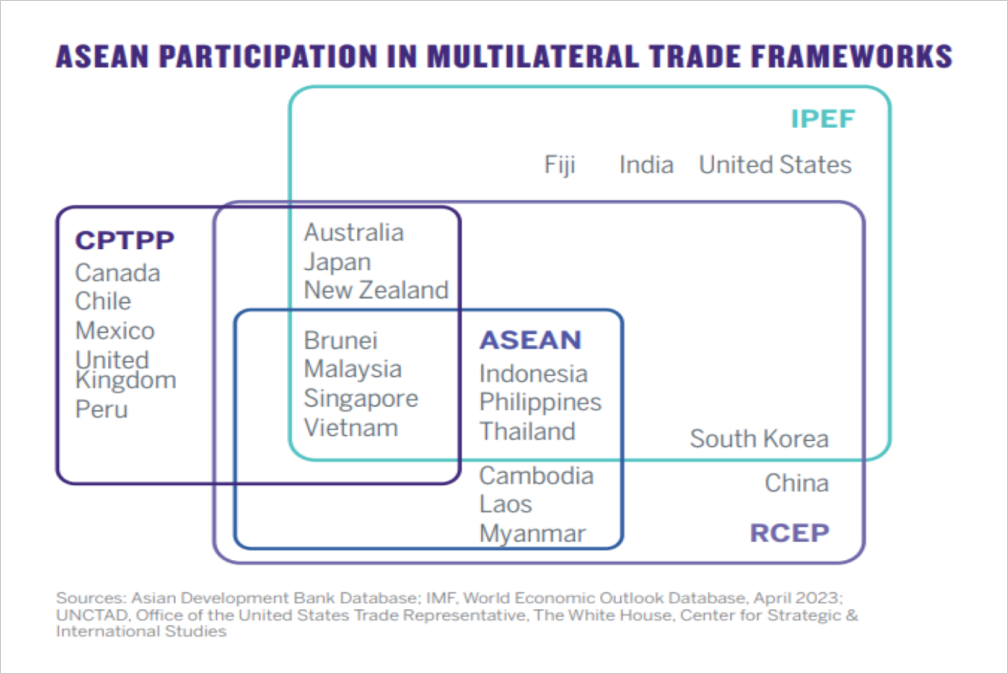

ASEAN is at the heart of a network of multilateral and bilateral free trade agreements (FTAs) in the Indo-Pacific region. ASEAN has FTAs in place with the region’s biggest economies including China, Japan, South Korea, India, Australia and New Zealand, and Hong Kong. Additionally, ASEAN also continues to negotiate FTAs, including with Canada.

While the United States does not have an FTA with ASEAN, economic ties were formalized with the US-ASEAN Trade and Investment Framework Agreement in 2006 and elaborated with the Expanded Economic Engagement Work Plan in 2012. The US Trade Representative also participates in annual consultations during the ASEAN Economic Ministers’ Meetings.

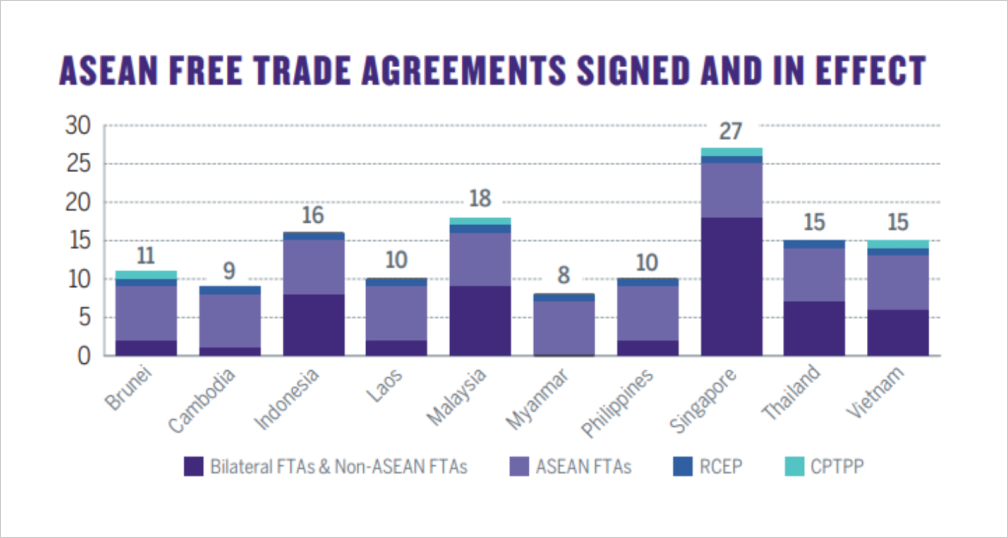

The 2004 US-Singapore Free Trade Agreement was America’s first FTA in the Indo-Pacific. Outside of multilateral FTAs, the 10 ASEAN member states are individually a part of 55 active FTAs. These network of FTAs are a key reason why several ASEAN member states are viewed as trusted trade partners playing vital roles in the global and regional supply chains.

ASEAN is central to the Regional Comprehensive Economic Partnership Agreement (RCEP), a FTA that includes all 10 ASEAN member states and five Indo-Pacific partners. Over 20 years, RCEP aims to eliminate about 90% of tariffs with exemptions for “sensitive” or “strategic” goods. It also contains a rules of origin provision that regards RCEP members as one economic region. RCEP is estimated to add $245 billion annually to regional income and 2.8 million jobs to the region by 2030.

Four ASEAN countries are also members of the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). The CPTPP extends beyond market access commitments to include environmental and labor protections, rules for state-owned enterprises, and support for small and medium-sized enterprises. The CPTPP has outstanding membership applications from six countries, including China and Taiwan.

In May 2022, President Biden, alongside regional partners, launched the flagship economic initiative of the US Indo-Pacific strategy called the Indo-Pacific Economic Framework for Prosperity (IPEF). The framework’s goal is to “advance resilience, sustainability, inclusiveness, economic growth, fairness, and competitiveness for [IPEF] economies.” While it is not a formal FTA, IPEF will focus on eliminating non-tariff barriers to trade to increase business opportunity and job growth across four strategic pillars: Trade; Supply Chains; Clean Energy, Decarbonization, and Infrastructure; and Tax and Anti-Corruption. In 2023, Indonesia and Singapore hosted the second and third IPEF negotiating rounds, respectively, followed by the IPEF Ministerial Meeting in Detroit, Michigan, which resulted in the substantial conclusion of the IPEF Supply Chain Agreement negotiations. Thailand and Malaysia are also hosting negotiating rounds in 2023.

2) Micro, Small and Medium-Sized Enterprises (MSMEs)

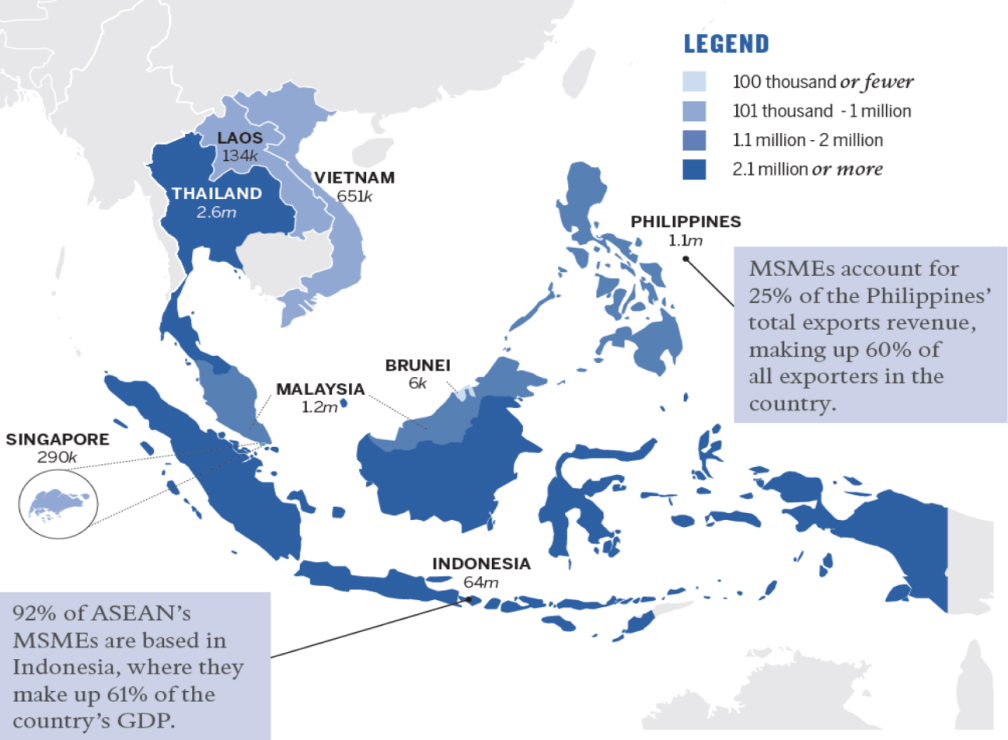

ASEAN is home to over 71 million MSMEs across eight member states (excluding Myanmar and Cambodia), employing a total of over 143 million people. MSMEs contribute to almost 45% of ASEAN’s GDP, 85% to employment, and 18% to its regional exports. They are predominant in ASEAN’s service sector, including retail, trade, and agricultural activities. However, MSMEs are facing challenges with respect to business integration in the region and global markets through global value chains.

In 2021, the number of MSMEs increased by 13% in the Philippines, 7% in Malaysia, and 3% in Singapore. With government support, 85% of Indonesia’s MSMEs reported their businesses have returned to normal after COVID-19 disruptions, and 22% of the MSMEs that closed during the pandemic have successfully reopened.

3) MSME Digital Economy Integration

Integration of MSMEs in the digital economy is predicted to add $3.1 trillion to the Indo-Pacific’s total GDP by 2024, including $30 billion to Vietnam’s GDP. Currently, just over 17 million of Indonesia’s 64 million MSMEs are participating in the digital economy. The government aims to expand participation to 30 million MSMEs by 2024. Malaysia’s target is to digitalize the business operations of 90% of its MSMEs by 2025.

In a survey of over 1,500 MSMEs across all 10 ASEAN member states, 80% of surveyed enterprises reported they had expanded their use of digital tools in the past two years, largely prompted by the COVID-19 pandemic. However, 65% of the MSMEs identified internet accessibility and affordability as barriers to their growth. Only one-third of the surveyed MSMEs reported using e-commerce platforms and marketplaces to conduct digital payments.

Supporting technology adoption and MSME e-commerce participation is a key strategic objective in the Master Plan for ASEAN Connectivity 2025. First launched in 2016 as the ASEAN SME Academy and updated in 2022, the ASEAN SME Academy 2.0 is a joint initiative between the US-ASEAN Business Council (USABC), USAID, and the ASEAN Coordinating Committee for MSMEs. As an official ASEAN platform, the Academy is co-administered by USABC, the Bureau of SME Development under Philippines Department of Trade and Industry, and the Philippines Trade and Training Centre. It is an online learning platform that provides trainings and resources for MSMEs on technologies for growth, financial products, regional and international markets, and more. The platform is available in four languages and includes courses on COVID-19 recovery. The program has over 5,600 active users from all 10 ASEAN member states, including almost 4,200 MSME participants.

ASEAN Economic Issues (December 2023)

1. 2023년 11월 수출입 동향

단위: 백만 불

| Country/Region |

November 2023 |

November 2022 |

2022 |

| Export |

Import |

Total |

Total |

Total |

| Total (Korea) |

55,776 |

51,998 |

107,775 |

110,620 |

1,414,954 |

| ASEAN |

9,824 |

6,126 |

15,950 |

15,227 |

207,418 |

| Brunei Darussalam |

7 |

121 |

127 |

5 |

345 |

| Cambodia |

47 |

38 |

86 |

71 |

1,051 |

| Indonesia |

812 |

897 |

1,708 |

1,921 |

25,951 |

| Lao PDR |

9 |

5 |

16 |

8 |

150 |

| Malaysia |

941 |

1,247 |

2,188 |

2,024 |

26,723 |

| Myanmar |

25 |

31 |

57 |

70 |

1,013 |

| Philippines |

763 |

403 |

1,166 |

1,232 |

17,484 |

| Singapore |

1,704 |

852 |

2,555 |

2,065 |

30,553 |

| Thailand |

590 |

536 |

1,125 |

1,235 |

16,461 |

| Vietnam |

4,926 |

1,994 |

6,921 |

6,596 |

87,688 |

| China |

11,356 |

12,086 |

23,442 |

23,507 |

310,366 |

| Japan |

2,565 |

3,718 |

6,283 |

6,615 |

85,318 |

출처: 관세청 (월별 업데이트)

(총괄) 한국 수출 558억 달러(7.8%), 수입 520억 달러(-11.6%), 무역수지 38억 달러 흑자 기록,

11월 수출은 올해 최대 수출 실적을 1개월만에 경신하며 2개월 연속 수출 플러스 달성

(국가별 수출) 대아세안 수출은 2개월 연속 증가흐름을 유지하였으며 대미국 수출은 역대 최고 실적인 109억 달러를 달성, 대중국 수출은 올해 최대 실적인 114억 달러 달성

(품목별 수출) 반도체 등 12개 품목 수출 증가, 플러스 품목 수 올해 최대

(주요 흑자국) 미국(47억 4천만 달러), 아세안(37억 달러), 베트남(29억 3천만 달러), 일본(11억 5천만 달러)

(평가 및 정책방향) 산업통상자원부 보도자료에 따르면 어려운 대외여건에도 불구하고 우리 수출과 무역수지 모두 올해 최대실적을 동시 기록하였으며, 고금리∙장기화로 어려움을 겪는 중소∙중견기업의 금융 부담 완화를 위해 ‘수출 패키지 우대보증’ 방안을 연내 마련하고 수출 상담∙전시회를 집중 개최하여 해외마케팅을 지원할 것임. (Link)

2. 2023년 3분기 해외직접투자 동향

투자금액(단위: 백만 불)

| Country/Region |

2022 |

2023 |

| Q1 |

Q2 |

Q3 |

Total |

Q1 |

Q2 |

Q3 |

Total |

| Total (Korea) |

28,221 |

19,845 |

18,374 |

66,440 |

16,893 |

15,649 |

14,623 |

47,165 |

| ASEAN |

2,219 |

2,248 |

1,667 |

6,133 |

1,267 |

2,316 |

1,499 |

5,082 |

| Brunei Darussalam |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

| Cambodia |

19 |

163 |

63 |

245 |

131 |

47 |

54 |

232 |

| Indonesia |

387 |

208 |

420 |

1,016 |

257 |

855 |

420 |

1,533 |

| Lao PDR |

19 |

31 |

9 |

59 |

3 |

9 |

13 |

26 |

| Malaysia |

167 |

52 |

108 |

328 |

64 |

48 |

51 |

164 |

| Myanmar |

112 |

88 |

101 |

301 |

45 |

56 |

38 |

139 |

| Philippines |

31 |

15 |

18 |

64 |

25 |

22 |

32 |

79 |

| Singapore |

1,034 |

799 |

388 |

2,220 |

243 |

399 |

237 |

880 |

| Thailand |

45 |

37 |

20 |

102 |

45 |

17 |

67 |

130 |

| Vietnam |

403 |

855 |

540 |

1,798 |

454 |

863 |

584 |

1,901 |

출처: 한국 수출입은행

(총괄) 2023년 3분기 우리나라 해외직접투자액(총투자기준)은 전년 동기(183.7억 달러) 대비 20.4% 감소한 146.2억 달러를 기록

(지역별) 2023년 3분기 모든 지역의 투자액은 전년 동기 대비 감소했으며 특히 아시아 지역은 작년 대비 43.8% 감소

(국가별) 아세안 국가 중에서는 베트남, 인도네시아 투자액이 전년 동기 대비 증가(각각 8.3%, 0.1%)했으나 상위 투자국인 싱가포르의 경우 28.8% 감소하였음. 상위 투자대상국으로는 66.8억 달러로 미국이 1위를 차지하였고 5.8억 달러의 베트남이 5위를 차지

(업종별) 투자액이 많은 업종으로는 금융보험업, 부동산업, 전문과학기술업 순

(분석) 3분기 해외직접투자액은 전분기에 이어 감소세를 지속했으며, 이는 주요국의 고금리 기조 및 유럽·중국 등의 경기둔화 우려 등이 영향을 미친 것으로 평가됨. 한편, 이차전지 시장 선점과 공급망 강화를 위한 북미·아세안 지역 관련 산업 투자가 지속되는 양상을 보이고 있으며, 對중국 투자는 위축세를 지속하고 있음.

3. ASEAN Matters for America/America Matters for ASEAN 발췌 (Link)

프로젝트 기관: East-West Center in Washington (Asia Matters for America Initiative)

협력 기관: US-ASEAN Business Council, ISEAS-Yusof Ishak Institute

1) 무역 협정과 프레임워크

아세안은 인도-태평양 지역의 다자간 그리고 양자간 자유 무역 협정 네트워크의 중심에 있음. 아세안은 중국, 일본, 한국, 인도, 호주와 뉴질랜드, 홍콩을 포함한 이 지역 최대의 경제국들과 FTA를 맺고 있으며 캐나다와도 FTA 협상을 진행 중에 있음.

미국은 아세안과 직접적인 FTA를 맺고 있지 않지만 2006년 미-아세안 무역투자 기본협정으로 경제관계를 공식화하고, 2012년 확장적 경제참여 업무계획(Expanded Economic Engagement Work Plan)을 구체화하였음. 미국 무역대표부의 경우 아세안 경제장관회의 동안 열리는 연례 회의에 참여함.

2004년 미국과 싱가포르 간의 자유무역협정은 인도·태평양 지역과 미국이 최초로 체결한 FTA로, 아세안 10개 회원국은 다자간 FTA 외에도 개별적으로 55개의 FTA를 체결하고 있음. 이러한 FTA 네트워크는 아세안 회원국들이 글로벌 및 역내 공급망에서 중요한 역할을 하며 다른 국가들이 신뢰할 수 있는 무역 파트너로 인식되는 핵심적인 이유로 여겨짐.

아세안은 10개의 아세안 회원국과 5개의 인도-태평양 협력국을 모두 포함하는 FTA인 역내포괄적경제동반자협정(RCEP)의 중심에 있음. RCEP는 20년에 걸쳐 회원국 90%의 상품관세 철폐를 목표로 하며 RCEP 회원국을 하나의 경제 지역으로 간주하는 원산지규정을 담고 있음. RCEP는 매년 해당 지역 소득에 2,450억 달러, 2030년까지 280만 개의 일자리를 기여할 것으로 추정됨.

아세안 4개국(브루나이, 말레이시아, 싱가포르, 베트남)은 또한 포괄적・점진적 환태평양경제동반자협정(CPTPP)의 회원국으로, 해당 협정은 시장 접근성을 넘어 환경 및 노동 보호, 국영기업 규칙, 중소기업 지원 등을 포함함. 관련해서 중국과 대만의 신청도 받은 상태임.

2022년 5월 미국은 역내 파트너들과 함께 ‘번영을 위한 인도·태평양 경제 프레임워크(IPEF)’라고 불리는 미국의 인도·태평양 전략의 대표적인 경제 이니셔티브를 시작하였음. 해당 프레임워크의 목표는 ‘회복력, 지속 가능성, 포괄성, 경제 성장, 공정성 및 IPEF 경제를 위한 경쟁력 향상’으로 공식적인 자유 무역 협정은 아니지만 IPEF는 무역, 공급망, 청정 에너지, 탈탄소화 및 인프라, 세금 및 반부패의 네 가지 전략적 축에서 사업 기회와 일자리 증가를 위해 무역에 대한 비관세 장벽 제거에 중점을 둠. 2023년에 인도네시아와 싱가포르는 각각 2차, 3차 IPEF 협상을 개최하고 미시간주 디트로이트에서 IPEF 장관 회의를 개최하여 IPEF 공급망 협정 협상의 실질적인 타결을 가져왔음. 태국과 말레이시아도 연내 성과 도출을 목표로 2023년 각각 5차, 6차 협상을 개최하였음.

2) 아세안의 중소기업

중소기업(MSME)은 아세안의 경제 성장에 매우 중요한 역할을 하며 각 회원국의 기업 97~99%를 대표함. 아세안에는 7,100만개 이상의 중소기업이 자리하고 있으며(8개 회원국 기준, 미얀마와 캄보디아 제외) 총 1억 4,300만 명 이상이 해당 기업에서 종사하고 있음. 이처럼 중소기업은 아세안 GDP의 약 45%, 고용의 85%, 지역 수출의 18%에 기여하고 있으며 리테일, 무역 및 농업 활동을 포함하여 아세안의 서비스 부문에서 압도적인 숫자에 해당함. 그러나 현재 중소기업들은 글로벌 가치 사슬을 통한 지역 및 글로벌 시장에서의 사업 통합과 관련하여 어려움을 겪고 있음.

2021년 중소기업의 수는 필리핀에서 13%, 말레이시아에서 7%, 싱가포르에서 3% 증가하였음. 인도네시아의 경우 팬데믹 이후 기업의 85%가 정부 지원을 통해 정상화되었고, 해당 기간 동안 문을 닫았던 중소기업의 22%가 성공적으로 영업을 재개하였음.

3) 중소기업과 디지털 경제

중소기업의 디지털 경제 실현을 통해 베트남 GDP에는 300억 달러, 인도∙태평양 지역에는 2024년까지 총 GDP에 3.1조 달러가 추가될 것으로 예상됨. 현재 인도네시아의 6,400만 중소기업 중 1,700만 개 정도의 기업들이 디지털 경제에 참여하고 있으며 인도네시아 정부는 2024년까지 3,000만 개로 확대하는 것을 목표로 하고 있음. 말레이시아의 경우 2025년까지 중소기업의 90%가 비즈니스 운영을 디지털화 하는 것을 목표로 함.

10개 아세안 회원국 1,500개 이상의 중소기업을 대상으로 한 설문조사에서, 응답자의 80%가 지난 2년 동안 팬데믹으로 인해 디지털 툴 사용 확대를 시도했다고 답하였음. 그러나 응답자의 65%는 인터넷 접근성과 가격 접근성을 어려움으로 뽑았으며 조사 대상의 1/3만이 디지털 결제를 통한 전자 상거래 플랫폼을 이용한다고 답변함.

기술 채택 및 중소기업 전자상거래 참여 지원은 ASEAN Connectivity Master Plan 2025의 핵심 전략 목표이기도 함. 그에 대한 예시로 ASEAN SME Academy는 2016년 처음 시작되어 2022년 ASEAN SME Academy 2.0로 업데이트 된 프로젝트로, US-ABC(US-ASEAN Business Council), USAID(U.S. Agency for International Development ), ACCMSME(ASEAN Coordinating Committee on Micro, Small and Medium Enterprises)의 공동 이니셔티브로 시작되었음. 아세안의 공식 온라인 플랫폼으로서 US-ABC, 필리핀 무역산업부 산하 중소기업개발국, 필리핀 무역훈련센터가 공동 관리하고 있음. 플랫폼을 통해 아세안 중소기업들에게 금융상품, 지역 및 국제 시장 등의 기술에 대한 교육 및 자원을 제공하며 여기에는 COVID-19 회복에 대한 강좌도 포함되어 있음. 플랫폼은 현재 총 4개 언어(영어, 태국어, 인도네시아어, 베트남어)로 제공되고, 아세안 10개국으로부터 5,600명 이상의 이용자를, 그 중에서도 약 4,200명의 중소기업 종사자를 보유하고 있음.

Latest ASEAN News국가별 주요 뉴스

ASEAN-KOREA CENTRE 한-아세안센터

ASEAN-KOREA CENTRE 한-아세안센터

ASEAN 아세안

ASEAN 아세안

Brunei Darussalam 브루나이

Brunei Darussalam 브루나이

Cambodia 캄보디아

Cambodia 캄보디아

Indonesia 인도네시아

Indonesia 인도네시아

Lao PDR 라오스

Lao PDR 라오스

Malaysia 말레이시아

Malaysia 말레이시아

Myanmar 미얀마

Myanmar 미얀마

Philippines 필리핀

Philippines 필리핀

Singapore 싱가포르

Singapore 싱가포르

Thailand 태국

Thailand 태국

Viet Nam 베트남

Viet Nam 베트남